We’ve only seen this happen six times since 1871, and the previous five cases have served as a warning to Wall Street and investors.

Since the start of 2023, Wall Street has been operating at full capacity. During this period of approximately 17.5 months, we observed mature equity-oriented markets. Dow Jones Industrial Average (^DJI -0.15%) gains 17%, the benchmark S&P500 (^GSPC -0.04%) add 42%, and fueled growth Nasdaq Composite (^IXIC 0.12%) catapult higher by 69%. More importantly, all three indexes reached record highs and firmly established themselves in bull markets.

On paper, things are going swimmingly for Wall Street. The majority of S&P 500 constituents beat consensus earnings expectations, and the U.S. economy remained on track. Despite some historically accurate predictors of a U.S. recession in 2023, the economy continues to grow.

But history also teaches us that the stock market rarely moves in a straight line for an extended period of time. While the hype around artificial intelligence (AI) is undoubtedly giving stocks a boost, it doesn’t eliminate the possibility that stocks will come back to Earth at some point in the future.

Image source: Getty Images.

While there is no foolproof metric when it comes to predicting short-term directional moves in the Dow Jones, S&P 500, and Nasdaq Composite, some predictive tools have an uncanny track record of correlating with big moves of the stock market throughout history. One such valuation indicator, which has 153 years of data in its sails, offers an important clue as to whether the stock market will collapse or not.

Are stocks headed for disaster?

Over the past year, I’ve looked at an assortment of predictive tools that are highly correlated with important directional moves in Wall Street’s three major stock indexes. These include the US Money Supply M2, the ISM New Manufacturing Orders Index, and the Conference Board Leading Economic Index (LEI), to name a few.

But if there’s one metric that has a long history of foreshadowing big moves on Wall Street more than any other, it’s the valuation-based Shiller price-to-earnings (P/E) ratio, which is also commonly called the cyclically adjusted ratio. price/earnings ratio or CAPE ratio.

With a traditional P/E ratio, a company’s stock price is divided by its earnings per share over the trailing 12 months. However, the Shiller P/E ratio of the S&P 500 is based on inflation-adjusted average earnings over the prior period. 10 years. Looking at a decade’s worth of earnings data helps eliminate one-off events, such as COVID-19, that can hamper valuation analysis.

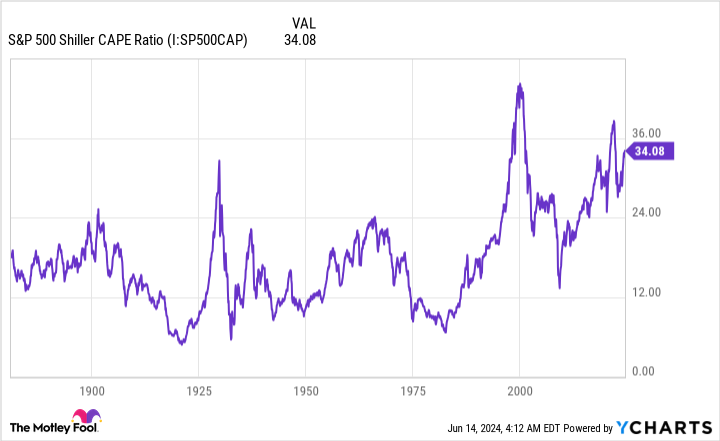

As of the June 13 close, the Shiller P/E for the S&P 500 stood at 35.38. When tested back in early 1871, this represents one of the highest figures ever recorded during a bull market rally. It’s also more than double the average over the past 153 years of 17.13 – although ease of access to public data (thanks, Internet!) and a period of historically low interest rates have certainly encouraged risk-taking and the expansion of earnings multiples over the last period. 30 years.

S&P 500 Shiller CAPE ratio data by YCharts.

However, Shiller’s P/E ratio, which is more than twice its historical average, is not the biggest concern. Rather, this is what followed every instance where the S&P 500’s Shiller P/E rose above 30 during a bull market rally:

- August 1929-September 1929: Immediately before the Great Depression took hold in the United States, Shiller’s P/E exceeded 30 for the first time. The Dow Jones would then lose 89% of its value before returning to its lowest point.

- June 1997-August 2001: During the dotcom bubble, the Shiller P/E of the S&P 500 reached its all-time high above 44. This was followed by the S&P 500 losing 49% and the Nasdaq Composite losing more than 75% from its summit.

- September 2017-November 2018: A 20% swoon in the S&P 500 in the fourth quarter followed another example of an extended rally pushing the Shiller P/E north of 30.

- December 2019-February 2020: In the months leading up to the COVID-19 crash, the Shiller P/E exceeded 30. The S&P 500 would lose 34% of its value in 33 calendar days during the COVID-19 crash of 2020.

- August 2020-May 2022: During the first week of January 2022, the Shiller P/E hit 40 for only the second time in its back-testing history. During the 2022 bear market, the S&P 500 would lose up to 28% of its value, with the Nasdaq taking an even harder hit.

- November 2023-current: As noted, Shiller’s P/E is currently above 35, as of June 13, 2024 close.

Shiller’s P/E ratio has exceeded 30 six times in 153 years, and the previous five instances were all associated with declines in the S&P 500, Dow, or Nasdaq Composite ranging from 20% to 89%. Based on what history has taught us about valuation expansion, a significant decline – and perhaps even a short-lived “crash” – could be expected.

Just keep in mind that the Shiller P/E is not a timing tool. As you will see during the dotcom bubble, stocks remained exceptionally expensive for over four years. The current stock market price could hold steady for weeks, months, or years before collapsing, as history suggests.

Image source: Getty Images.

History is a two-sided coin that strongly favors long-term optimists

The prospect of a bear market or stock market crash probably isn’t something you want to hear with the Nasdaq Composite, S&P 500 and Dow Jones Industrial Average in full rally mode. But the good news I have to offer you is that the story is not linear and is more on the side of optimistic investors who invest their money with a long-term horizon in mind.

To be honest, nothing we do, say or think as investors can prevent economic recessions or occasional downturns (corrections, bear markets or crashes) in the stock market. These declines are a natural part of the economic cycle and long-term investing.

There is, however, a marked difference between periods of growth and contraction in the U.S. economy. Since the end of World War II in September 1945, nine of twelve U.S. recessions have been resolved in less than twelve months. Of the other three, none lasted more than 18 months.

On the other side of this disproportionate coin, most economic expansions have been going on for many years. In fact, two growth periods since the end of World War II have exceeded the ten-year mark. If you are an investor, betting on the growth of the US economy over time is absolutely the right move.

We also see these same disparities between bear and bull markets on Wall Street.

It’s official. A new bull market is confirmed.

The S&P 500 is now up 20% from its closing low on 10/12/22. The previous bear market saw the index fall 25.4% over 282 days.

Learn more at https://t.co/H4p1RcpfIn. pic.twitter.com/tnRz1wdonp

— Custom (@bespokeinvest) June 8, 2023

A year ago, researchers at Bespoke Investment Group released a data set on of the Great Depression in September. 1929. This analysis covered 27 separate bear and bull markets, as you can see in the article.

While the average S&P 500 bear market lasted about 9.5 months (286 calendar days), the typical bull market lasted 1,011 calendar days, or about 3.5 times longer. Additionally, 13 bull markets have lasted longer than the longest bear market of over 94 years.

In the short term, the directional movements of the Dow Jones, S&P 500 and Nasdaq Composite will always be somewhat unpredictable. While a crash remains possible, given what history tells us about stock valuations, historical data on stock returns and economic growth clearly show that being optimistic and investing for the long term is a winning formula.