Jonathan’s Kitchen

We have already talked about Alphabet Inc. aka Google (NASDAQ: GOOG) in May 2024, discussing its promising outlook in search engine/generative AI capabilities, as well as robust profitability and a strong balance sheet in Q1 2024.

Combined with its ability to In order to ensure continued profitable growth and solid returns for shareholders, we then raised our rating from buy to “strong buy”, the stock being still fairly valued while offering excellent upside potential.

Since then, GOOG has gained another +16.1%, significantly outperforming the broader market at +8.4%, before the recent rotation away from high-growth stocks over the past two weeks.

Still, we remain optimistic about its long-term outlook, driven by its double-high Q2 2024 earnings call and accelerating cloud performance metrics.

Coupled with relatively cheap P/E valuations compared to its Magnificent 7/streaming/autonomous driving peers, it goes without saying that The stock remains a long-term winner for growth-oriented investors.

We will discuss this in more detail.

GOOG’s investment thesis in embedded AI has been handsomely rewarded

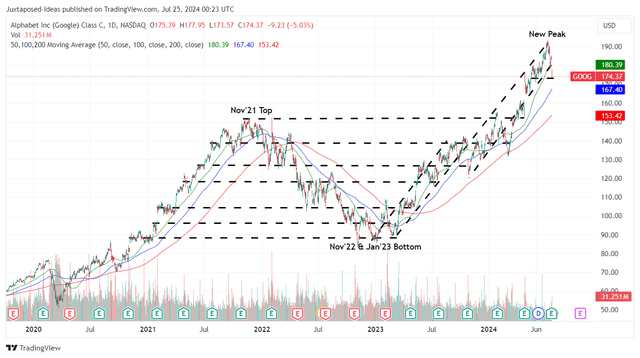

GOOG 3Y Stock Price

TradingView

GOOG has had a volatile three years, as observed in the stock price chart above, attributed to the pre-pandemic boom, the subsequent correction after November 2021, and the eventual recovery from the January 2023 trough.

Despite previous market concerns about the longevity of its Google Search segment, as noted in our GOOG article here in January 2023, it is clear that these fears were unfounded.

That is why.

GOOG continues to hold the largest global search engine market share of 91.06% in June 2024 (+0.26 points MoM / -1.58 YoY / -1.65 points from December 2019 levels of 92.71%), despite minimal share losses from November 2022 levels of 92.21% when ChatGPT launched.

While some of the losses are attributed to Microsoft (MSFT) Bing gains, we are not overly concerned, as Google Search continues to generate impressive revenues of $48.5 billion in Q2 2024 (+5% qoq / +13.7% yoy / +105.1% from Q2 2019 levels of $23.64 billion).

At the same time, GOOG is also moving closer to its projected $100 billion in revenue from both YouTube Ads and Google Cloud by the end of 2024, as seen in Q2 2024 cumulative revenue of $19 billion (+7.5% qoq / +21% yoy / +233.5% from Q2 2019 levels of $5.7 billion).

More importantly, management has demonstrated its ability to propel Google Cloud to sustainable profitability, despite our initial skepticism about the new accounting methodology, attributed to the “extended useful life of its servers by four to six years and its networking equipment by five to six years.”

This led to an increase in Google Cloud’s operating margins of 11.3% in Q2 2024 (+1.9 points QoQ / +6.4 YoY), further highlighting why their continued innovation across every layer of the AI stack has paid off handsomely.

This is also why we believe that as an AI-driven company, GOOG has demonstrated strong monetization efforts in its search/generative AI/cloud offerings, through its multi-modal embedded AI capabilities, which in turn improve user experience and increase search engine loyalty.

We should remind readers that GOOG has an in-house AI team unlike Microsoft’s partnership with OpenAI, which allows the former to vertically integrate platform building expertise while innovating in its existing/new offerings.

This further underscores why management was able to quickly deploy/monetize Gemini across its development tools and data centers to edge use cases.

Combined with the continued rationalization of its offerings and workforce, it is not surprising that we have seen GOOG’s strong revenue growth translate into increasingly rich adjusted operating margins of 32.3% (+0.7 points qoq / +3.1 yoy / +8.8 from 23.5% in Q2’19) in Q2’24.

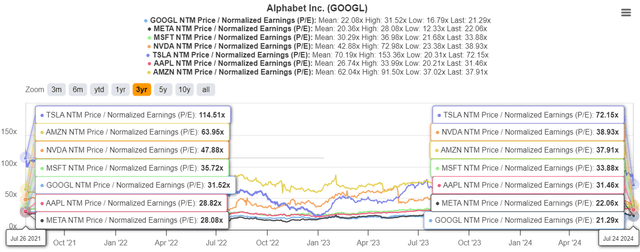

GOOG Reviews

Tikr Terminal

With forward consensus estimates holding steady over the past three months and GOOG still expected to report accelerating revenue/net income expansion at a CAGR of +11.6%/+19.4% through FY2026, it’s clear that the stock remains cheap here.

This is especially true since GOOG, with a FWD P/E valuation of 21.29x, still trades well below its Magnificent 7 peers (with the exception of META at 22.06x) and its 5-year average P/E of 25x, as observed in the chart above.

Even when compared to their net growth rates, such as Meta at 22.06x at +20.9% through FY2026, AAPL at 31.46x/ +10.3%, MSFT at 33.88x/ +16.5%, AMZN at 37.91x/ +37.5%, NVDA at 38.93x/ +49.6% and TSLA at 72.15x/ +13.3%, respectively, it is evident that GOOG is on the cheap side compared to Mag 7’s other peers.

Given YouTube’s streaming market share of 8.4% in June 2024 (+0.8 points m/m / +0.2 y/y) in an overall market growing by 40.3% (+1.5 points m/m / +2.6 y/y), it is clear that the secular shift from TV media to streaming is still underway.

Even compared to its streaming peer, Netflix (NFLX) with FWD P/E valuations of 33.57x with projected adjusted EPS growth of +31.1% through FY2026, it is clear that GOOG remains very attractive at current levels.

Finally, readers should not forget GOOG’s self-driving capability, Waymo, which has begun offering more than 50,000 paid public rides per week in San Francisco and Phoenix, as well as its ongoing fully autonomous (driverless) testing.

While TSLA has touted the capabilities of robo-taxis with an event now scheduled for October 10, 2024, it remains to be seen when monetization can actually take place, with Waymo currently leading the race.

Following these developments, we maintain our belief that the market is sleeping on GOOG’s well-diversified capabilities, providing interested investors with an excellent margin of safety despite the massive rally since the January 2023 low.

So, is GOOG stock a buy?Sell or keep?

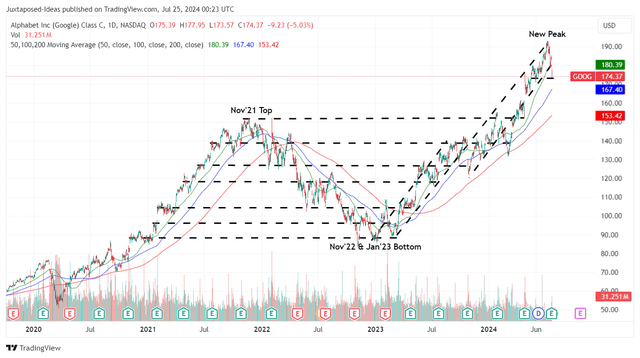

GOOG 3Y Stock Price

TradingView

For now, GOOG has hit a new high of $190 and is trading above its 100/200-day moving averages, driven by strong Q2 2024 results and market conviction around its AI monetization.

Despite the recent correction, the stock continues to trade not too far from our previous article levels of $170, with current levels still close to our updated fair value estimates of $174.20, based on LTM adjusted EPS of $6.97 (+6.9% from previous levels of $6.52) and 5-year P/E valuations of 25x.

At the same time, there remains excellent upside potential of +40.6% to our reiterated long-term price target of $258.30, based on stable consensus estimates for FY2026 adjusted EPS.

Additionally, GOOG has executed well on its long-term shareholder returns, based on the 269 million shares, equivalent to 2.1% of its float retired during the LTM, and 1.35 billion / 9.7% since FY2019, with approximately $54 billion still remaining in its repurchase authorization.

Although small, the annualized dividend of $0.80 per share allows long-term shareholders to DRIP and accumulate additional shares on a quarterly basis.

Given its strong AI monetization prospects and potential dual-track returns via capital appreciation and dividend payouts, we maintain our Buy rating on GOOG stock here.

Don’t sleep on this giant.